The rise and fall of Magic Eden from dominant NFT marketplace to target of massive class action litigation tells a complete story about crypto fraud, strategy changes driven by red numbers, and consumers trapped in unfulfilled promises. In June 2026, three plaintiffs filed legal action exposing how $ME token buyers received guarantees the company never delivered, and how subsequent pivots turned those promises to ash.

The Legal Case: Specific Actions, Specific Promises

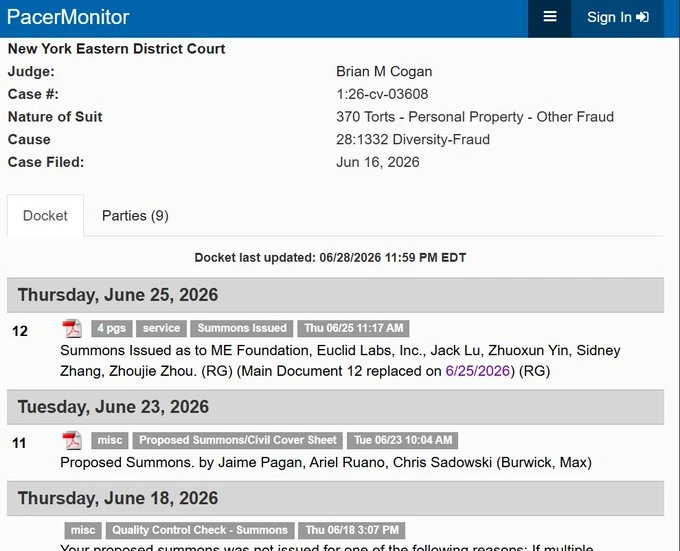

The lawsuit (Case No. 1:26-cv-3608) was filed by Jaime Pagan, Ariel Ruano, and Chris Sadowski on June 16, 2026 in U.S. District Court for the Eastern District of New York. Plaintiffs identified founders Jack Lu, Zhuoxun Yin, Sidney Zhang, and Zhuojie Zhou, as well as Euclid Labs Inc. (operating as Magic Eden) and ME Foundation.

What matters is not vague allegations—it is specific allegations. Plaintiffs assert that Magic Eden promoted $ME with guarantees that it would have real use cases within an expanding ecosystem, that it would function across multiple blockchain networks, provide voting power through ME DAO governance, reward users for trading or locking tokens, participate in revenue-sharing and buyback programs, and serve as the economic engine of the platform.

Those were not speculation. They were communicated directly through official materials, founder interviews, social media campaigns, and listings on major exchanges like Binance and Coinbase. Users bought based on those explicit premises.

What Never Materialized: Timeline of Broken Commitments

The multi-chain strategy—initially described as central to $ME’s value—was abandoned when Magic Eden announced it would refocus operations solely on Solana, discontinuing support for Bitcoin and Ethereum. Governance voting did not function operationally until nine months after launch. Revenue-sharing mechanisms were introduced only after significant delays. Staking rewards did not match initial descriptions. Trading rewards limited to seasonal allocations rather than continuous incentives. And the proprietary wallet required to claim tokens was later shut down over security concerns.

But there is more. Internal data revealed that 80% of Magic Eden’s costs were tied to products generating only 20% of revenue. Solana accounted for over 85% of total platform volume. The multi-chain expansion—once celebrated as Magic Eden’s defining evolution—had become an expensive bet that the market never fully sustained.

The Pivot to Dicey: From NFTs to Crypto Gambling

The true break came on February 27, 2026. Jack Lu announced that Magic Eden would shut down its Bitcoin Ordinals, Runes, and EVM NFT marketplaces entirely, sunset its multi-chain wallet, and refocus the company on two things: its Solana marketplace and Dicey—a new crypto gambling and iGaming platform.

Dicey was not an abstract announcement. Approximately 200 users wagered over $15 million in just two months of closed beta, leading Lu to describe iGaming as “a massive opportunity” deserving the company’s full resources alongside its Solana core.

But the logic governing that decision had implications for $ME. Consumers who bought tokens assuming Magic Eden would remain a multi-chain NFT company with operational governance now found the company betting its future on a crypto casino. The token’s value proposition shifted radically, without holder consent.

The legal response was immediate. A law firm (Burwick Law) announced it was investigating the ME token following the pivot, citing potential concerns around the token’s value proposition given the strategic reversal.

That occurred after the original lawsuit was already underway. What that means is clear: Magic Eden’s strategic shift did not only generate an existing legal case—it likely generates more.

The Token Unlock Shock: Upcoming Selling Pressure

Problems do not end with the lawsuit. Approximately 172.03 million ME tokens (17.2% of total supply) are scheduled to be unlocked on June 10, 2026, primarily for early contributors. Such events typically lead to increased selling pressure, especially in weak market conditions, potentially creating downside pressure on the token’s price.

Timing is brutal. Early investors gain liquidity exactly when:

- The legal case is underway

- The company has inverted its fundamental value proposition

- The broader crypto market is weak

- Users who bought at the peak see erosion of utility

Even the terms of what Magic Eden did maintain changed. Magic Eden overhauled its revenue-sharing mechanic, replacing 30% revenue allocation for token buybacks with a 15% split between $ME buybacks and USDC rewards for $ME stakers, effective February 1, 2026.

What that signals to plaintiffs is important: Magic Eden acknowledges its original commitments are not sustainable. The company is modifying terms—implicitly admitting that what it promised does not align with operational reality.

Plaintiffs describe three categories of harm suffered by those who acquired or held $ME: overpayment at purchase due to inflated expectations about use-case-driven demand; holding-period losses from retaining tokens based on ongoing representations; and restitutionary injury from providing economic benefits (such as liquidity or data) without receiving the represented product.

That covers the full spectrum of how fraud harms buyers:

- Initial overpayment: purchased at inflated prices based on promises

- Progressive dilution: retained expecting promises to be fulfilled

- Unpaid benefits: provided activity (volume, liquidity) that benefitted Magic Eden

Legal Foundation: Consumer Protection, Not Securities Law

The lawsuit does not seek judgment under securities law but instead relies on New York consumer protection statutes (General Business Law Sections 349 and 350) along with common-law claims of negligent misrepresentation and unjust enrichment.

Consumer protection laws have lower bars than securities law. “Deceptive representations” is far easier to demonstrate than “securities fraud.” Magic Eden made specific representations. Then did not fulfill them. The company changed the product’s value proposition. Plaintiffs can argue it is pure consumer protection.

Parallels with Celsius and FTX: The Pattern

Magic Eden joins a broader wave. Celsius promised staking yields. Turned out to be a Ponzi scheme. Celsius customers now receive recovery between 60% and 85% of their claims.

FTX promised security and liquidity. Was massive fraud. Creditors receive up to 119% of claimed amounts because Bitcoin appreciated.

Magic Eden promised operational governance, revenue-sharing, and multi-chain support. Then:

- Discontinued governance for 9 months

- Modified revenue-sharing

- Abandoned multi-chain support entirely

The pattern is consistent: grandiose promises during bull markets, non-delivery during bear markets, and customers trapped in between.

$ME price reflects reality. It spiked to $1.6 billion market cap in opening trading hours. Then fell below $1 billion within 20 minutes.

Users who gained access to claim early won. Those who faced technical issues (“something went wrong” errors, systems saying they already claimed when they had not) lost the window. Those who bought after the initial spike are underwater.

The June 2026 token unlock potentially makes things worse. When early investors gain liquidity exactly when the company faces massive litigation, selling probably will be fierce.

Magic Eden is not singular. It shows a reproducible pattern in crypto

First: platforms promise grandiose features to drive token purchases during strong markets. Second: when revenue falls (because markets cool), the company discovers promises are not economically viable. Third: they modify or abandon those promises. Fourth: investors get trapped.

What is missing is initial honesty. If Magic Eden had said

“We will launch primarily on Solana, with limited support for other chains, and we will adapt our strategy to where demand exists,” plaintiffs would have a weaker case.

But it is hard to buy tokens on “we may completely change our roadmap.”